Venture Capital Funding Trends & The Emergence of Secondary Funds

This blog post aims to discuss the current trends in the VC ecosystem in relation to capital flow and why the secondary market in VC may experience explosive growth over the coming years.

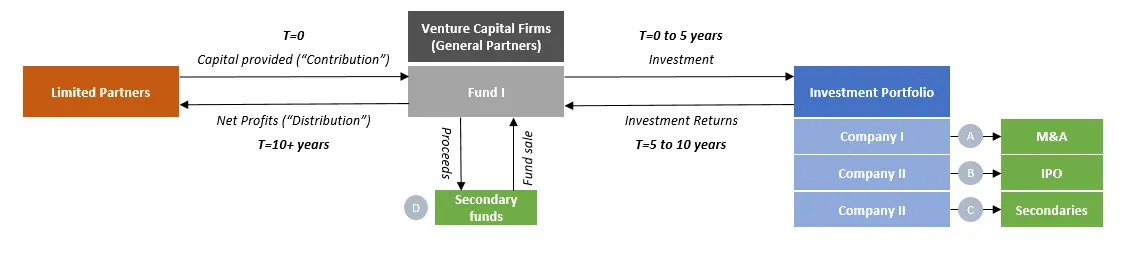

How Does capital flow in the VC ecosystem?

The graphic above illustrates the VC ecosystem. Limited Partners provide capital to VC funds, managed by VC firms (“General Partners”). The capital is deployed by General Partners to startups, which constitute the VC investment portfolio. Amid a liquidity event (IPO, M&A or secondaries), the VC fund exits its entire or partial stake in its investment and receives proceeds from the exit. The investment holding period (initial investment to exit) for VCs is typically 6–10 years and has increased over time.

In order to understand each trend within the ecosystem, it is important to view them as components of a wider system.

Relationship between Limited Partners and General Partners

Trend 1A: Capital provided to Venture Capital (“Contribution”) by Limited Partners Has Increased

The chart illustrates that the global VC cash flows over time. Since 2012, the global VC industry has received positive net capital inflow by Limited Partners of c.$151bn since 2012. In specific, the VC sector has received c.$441bn of new capital and distributed c.290bn to LPs since 2012. According to Goldman Sachs, VC dry powder reached a record level of more than $121bn in 2017. The level of investments into Venture Capital as an asset class are not surprising as the time period shown coincides with a global bull cycle, primarily driven by technology companies.

Relationship between General Partners and Investment Portfolio

Trend 1B: VC Investments Have Reached Record Levels

VC firms have been busy deploying capital, received by the Limited Partners. Since 2012, they have deployed c.$485bn in companies with a peak of $84bn in 2018.

Trend 2A: VC Exit Activity Has Declined relative to capital raised, partially driven by the availability of private capital

Due to (a) the availability of excess capital to VCs and (b) VC’s rate of capital deployment, VC-backed companies are able to raise late-stage funding rounds and so stay private / independent longer than in previous cycles. This has led to a reduction in exit activity over time relative to VC investments. Since 2012, the aggregate exit value on an annual basis is c.$89bn. The exit is predominantly achieved via IPO or acquisition with the composition changing over time.

Trend 2B: VC Investment Holding Period Have Increased

As companies stay private longer, VC investment holding period has increased significantly from 6.3 (4.2) years for exit via IPO (Acquisition/Buyout) in 2010 to 8.3 (4.9) years for exit via IPO (Acquisition/Buyout) in 2016. Whilst there is no data for 2017 and 2018, anecdotal evidence indicates that the holding period has increased since 2016.

What if Limited Partners / General Partners Become Impatient?

Despite increase in holding period, the dynamics between both LPs and GPs seem to be in tact as GPs are able to raise funds in just 2.4 years on average in 2018 vs. 3.3 years in 2006.

However, if the pressure to distribute returns increases in the future, VCs, confronted with ageing portfolio, would need to focus on achieving liquidity.

The primary exit options are (A) IPO and (B) M&A. Given the current stock market meltdown, driven by the tech sector, IPO and M&A activity are expected to cool down in the short to medium term. The third potential exit option would be (C) achieving liquidity through the secondary markets.

The Rise of the Secondary Market in Venture Capital

Rise of the Secondary Market

While secondary funds are common in Private Equity, its existence in Venture Capital has been “marginal” in the past. In 2018, capital invested in global VC secondary markets reached $10.8bn, primarily driven by SoftBank’s $8bn secondary transaction with Uber’s shareholders. Ignoring the activity in 2018, which is skewed by the SoftBank transaction, activity in the secondary market is very small relative to the traditional exit activity in the IPO / M&A market (see Trend 2A).

However, , secondary exits may become common in the near future as VC funds / LPs may as well as employees not patient enough to wait for another cycle to exit their investments.

Predictions for the Secondary Market

My predictions for the secondary market in VC are as follows. Driven by demand for liquidity by early investors and employees, we may see:

- Continued emergence of VC secondary funds and positive fundraising dynamics for secondary vehicles

- PE-focused secondary funds investing in the VC secondary market

- Secondary marketplaces such as Equidate, Equityzen, SharesPost may experience unprecedented growth and also expand to facilitate transactions among institutional investors

- Crowdfunding providers will further expand into facilitating secondary transactions. As an example, Seedrs has already started creating a secondary market to let its users buy or sell shares in private companies.

Key Stats

Notable Secondary Transactions (C)

- Jan-18: SoftBank / Uber (founded in 2009); $8bn secondary deal with existing investors including Benchmark Capital, First Round Capital, Menlo Ventures and management

- Mar-18: Silver Lake / Credit Karma (founded in 2007); $500m secondary investment to provide liquidity to investors and early employees

- Jul-18: Francisco Partners & GPI Capital / LegalZoom (2001); $500m secondary investment

Notable Fund Sale (D)

- Oct-17: Draper Espirit acquired Seedcamp’s Fund I & II for €20m, delivering 4x returns to Seedcamp’s investors

- Nov-18: NEA’s spin-out of NewView Capital with LPs including GS and Hamilton Lane

Notable Secondary Funds

- Balderton Capital: In 2018, it raised a $145m fund dedicated to secondary transactions in European companies

- Draper Espirit: very active as secondary tech investor in Europe

- 137 Ventures: US-based secondary fund, invested in Wish, SpaceX, Flexport, Gusto, DiDi

- Industry Ventures: US-based secondary fund with investments in ventures funds such as Battery Ventures, Draper Espirit, Lightspeed Venture Partners as well as companies including Alert Logic, Cambridge Display